- FTSE 100 index eases 23 points

- SIMEC Atlantis the top riser after financing deal

- Cadence Minerals tumbles after discounted share issue

3.35pm: After an early afternoon dive, the Footsie is rallying and attempting to regain the 6,000 level.

Londons index of top shares was down 23 points (0.4%) at 5,990.

The top riser in London was SIMEC Atlantis Energy Ltd (LON:SAE), which was up 49% at 26.5p, after it secure a £170mln loan to fund the first phase of its Uskmouth power station conversion project.

The biggest faller was Cadence Minerals PLC (LON:KDNC), down 17% at 13.5p after it raised £1.25mln by placing shares at 12p a pop.

SIMEC Atlantis Energy inks debt financing deal for Uskmouth project https://t.co/NPgnm0nNps #MasterEnergy

— MasterEnergy (@MasterEnergyRSS) August 21, 2020

3.30pm/10.30am EST: Proactive North America headlines:

Gevo Inc (NASDAQ:GEVO) secures $50 million at-the-market offering to pay down debt

Medallion Resources Ltd (CVE:MDL) (OTCPINK:MLLOF) upsizes private placing to C$1.6M due to market demand

Hillcrest Petroleum Ltd (CVE:HRH) (OTCMKTS:HLRTF) hires New York-based capital and advisory group to accelerate its business aims

Ximen Mining Corp (CVE:XIM) (OTCQB:XXMMF) updates on new portal work at Kenville gold mine project and reports positive metallurgical test results

Tiziana Life Sciences (LON:TILS, NASDAQ:TLSA) lands US patent for liver cancer drug in combination with tyrosine kinase inhibitors

Sorrento Therapeutics Inc (NASDAQ:SRNE) to take on start-up SmartPharm in an all-paper deal worth US$19.4mln

Phunware Inc (NASDAQ:PHUN) launches global reseller programme to support sales of enterprise mobile software

Versus Systems Inc (CSE:VC) (OTCQB:VRSSF) taps New York Media veteran David Spiegel to its advisory board

2.45pm: Negative start for Wall Street

The US markets have opened started Fridays session on the back foot, with all three of the main indices slipping into the red in the early minutes of trading.

Shortly after the opening bell, the Dow Jones Industrial Average was down 0.12% at 27,706, while the S&P 500 fell 0.03% to 3,384. The Nasdaq also dropped 0.02% to 11,262 despite briefly moving into positive territory in the opening minutes of the session.

Any optimism among traders may have been snuffed out following news that the USs daily coronavirus death toll have remained above 1,000 for the third day in a row.

Back in London, the FTSE 100 had recovered some of its losses and was down 30 points at 5,982 just after 2.45pm.

2.00pm: Footsie's losses lengthen despite sterling's travails

After a dull morning, Londons leading shares have trekked south with just 10 Footsie constituents clinging on to earlier gains.

The FTSE 100 was down 55 points (0.9%) at 5,958, despite sterling taking a mullering from the greenback on the foreign exchange markets.

The pound was down by more than a cent at US$1.3098.

12.15pm: NASDAQ party to continue but other US indices set for a subdued start

After making progress yesterday, US indices – except the NASDAQ Composite, of course – are expected to give back some of those gains today.

According to spread betting quotes, the Dow is expected to open 59 points lower at 27,681 and the S&P 500 6 points softer at 3,379.

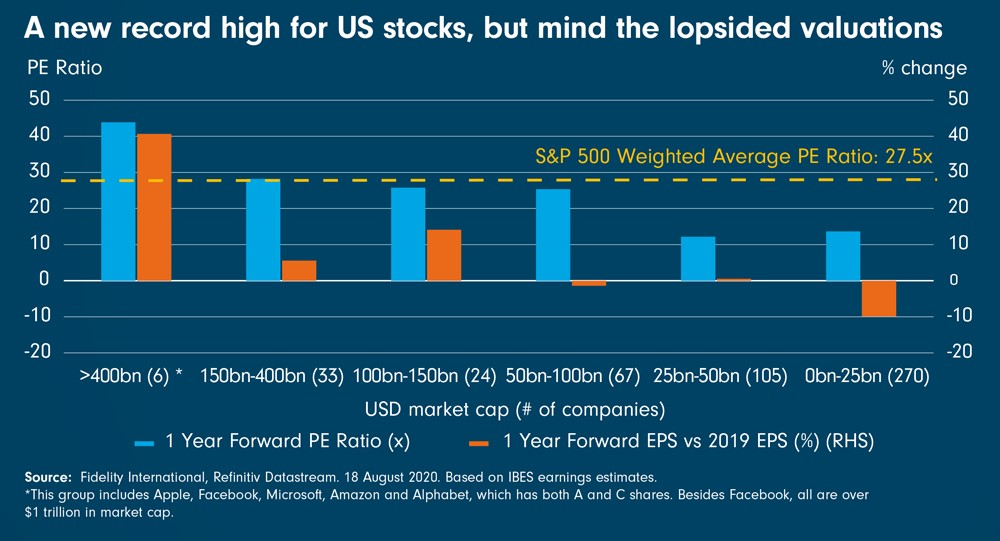

The tech-heavy NASDAQ is seen starting 202 points firmer at 11,467, driven by continued enthusiasm for the tech titans, for reasons explained by Stuart Rumble, an investment director at Fidelity International.

“The five biggest tech giants with over $400 billion market cap (Apple, Amazon, Microsoft, Facebook and Alphabet) continue to lead this rally and dominate the S&P 500. Their combined market cap is around $7 trillion and as a group now represent 23 per cent of the index based on market capitalisation, the biggest share in modern times for the top five. The tech titans also have the richest average PE ratio, at 44 times earnings. This significantly skews the entire indexs PE [price/earnings] ratio,” said Rumble.

“But dig a little deeper and a different picture starts to emerge. If we exclude the tech giants, the weighted average PE ratio of the remaining 495 index constituents is 22 times earnings. Still high, but much more reasonable. However, there is more to it than that.

“The market is putting a significant premium on earnings growth. This is clear when we compare todays estimates for 1-year earnings versus 2019 earnings. The weighted average growth in earnings 1 year from today is expected to be 41% higher than 2019 earnings for the top 5 largest companies, whereas it is essentially flat for the rest of the index.

“So, the message from the market is that the top five companies can keep driving growth while the rest of the index companies lag. We think this implies ample room for a broadening of the rally, but it is difficult to see that happening without a better macro outlook leading to a more widespread improvement in earnings forecasts,” Rumble ruminated.

Europe has had its purchasing managers indices (PMI) for August and the US will follow suit this afternoon. Economists, who are obliged to make predictions that do their reputations few favours, are expecting the manufacturing PMI to creep up to 52 and the services PMI to nudge up to 51.

“On the earnings front we have the latest Q3 [third quarter] numbers from US agricultural equipment company Deere and Co,” writes Michael Hewson of CMC Markets.

“Expectations are for profits to come in at $1.21c a share,” he added.

In the UK, the FTSE 100 looks like it is having a duvet day. The index is down 9 points (0.2%) at 6,005, despite the fact sterling has tanked against the dollar on foreign exchange markets. The pound is down seven-tenths of a cent at US$1.4144 as hopes fade of a Brexit agreement being clinched soon/this month/this year/this century [delete according to your level of cynicism[.

11.40am: CBI survey indicates output volumes continue to fall in August

Manufacturer output volumes in the three months to August continued to fall quickly, according to the CBI monthly Industrial Trends Survey.

On the plus side, the pace of decline eased a little from last months record decline.

The Total Order Books component of the survey improved to -46% in August from -59% in July.

The survey of 278 manufacturers found that output volumes declined in 16 of 17 sub-sectors, with the headline drop in output being primarily driven by the mechanical engineering, food, drink & tobacco, and motor vehicles & transport equipment sub-sectors.

According to the survey, manufacturers expect output to fall at a much slower pace (-10%) in the next three months. Firms also anticipate output prices in the next three months to fall at a modest pace (-5%).

“This has been another difficult month for manufacturers. Activity continues to be poor and order books severely depressed, although the worst of the decline seems to be behind us,” declared Anna Leach, the CBIs deputy chief economist.

“It is a relief to see the pressure on manufacturers starting to ease. As the sector looks to rebuild from the economic shock, the Government must consider additional ways to support this sector to help reinforce a recovery, such as grants and further business rates relief.

“As we head into the autumn months, a coherent plan to ensure the manufacturing sector is resilient to a potential second wave and to the challenge of adapting to a new trading relationship with the EU is vital,” she added.

The FTSE has battled – if thats the right word – its way back to par at 6,013.

10.30am: "A jobless recovery can only go so far"

The Footsie continues its crab-like shuffle as pundits sift through the ins and outs of the latest IHS Markit/CIPS purchasing managers indices (PMIs).

Londons index of leading shares was down 18 points (0.3%) at 5,995, – a level it has been clinging to since the release of the PMIs.

August flash #PMI shows #UK #manufacturing & #services activity up to 82-month high boding well for Q3 growth; composite output index up to 60.3 (57.0 in July; 47.7 in June). Services PMI at 72-month high of 60.1 (56.5 in July; manufacturing PMI at 30-month high of 55.3 (53.3)

— Howard Archer (@HowardArcherUK) August 21, 2020

The PMIs were generally moving in the right direction but private sector firms reported another sharp fall in employment numbers.

“The rate of job shedding accelerated since July, with survey respondents frequently noting that redundancy programmes had been running in tandem with efforts to return some staff from furlough,” revealed Tim Moore, the economics director at IHS Markit.

Duncan Brock, the group director at the Chartered Institute Institute of Purchasing & Supply (CIPS) reckons that the UK is heading for the deepest recession in living and that any celebrations following the latest PMI readings would be premature.

“Reducing headcount was a quick fix for many firms struggling to maintain strong supply chains and their position in the marketplace amidst higher raw material and import costs.

"With the fastest rise in activity in the private sector since October 2013, this shows an encouraging speed towards recovery which belies the fact there are still some dark forces at play. Rising inflation, the sustainability of the UK economy during a global pandemic and the poor employment figures means were not out of the woods yet," Brock said.

To put it another way, and to quote Samuel Tombs at Pantheon Macroeconomics, “a jobless recovery can only go so far”.

“The further rise in the composite PMI in August suggests that the economic recovery has broadly maintained the strong pace set in June when GDP rose by 8.7% month-to-month. With GDP still 17% below its pre-Covid level in June, it has scope to recover rapidly for a couple of months. Nonetheless, the slump in the composite PMI to 51.6 in August, from 54.9 in July, in the Eurozone, where the rebound is roughly one month further advanced, suggests that the UKs recovery soon will lose momentum too, at a point when GDP still is well below its pre-COVID peak,” Tombs said.

“In addition, the slightly lower level of the composite orders balance, 59.3, than the composite PMI suggests that economic activity currently is being supported by firms depleting work backlogs that had built up during the lockdown. Output in the manufacturing sector might fall outright in the autumn, if new orders do not pick up enough. Meanwhile, firms still are pushing though painful job cuts; the employment index dropped to 38.7 in August, from 39.6 in July, consistent with employee numbers falling at a 1.2% quarter-on-quarter rate in Q3. Accordingly, we continue to expect GDP to be about 5% below its pre-COVID level in Q4,” he added.

10.00am: UK PMI for August rises at fastest pace since October 2013

The IHS Markit Composite Purchasing Managers Index (PMI) for August rose to 60.3 from 57.0 in July.

IHS Markit observed that Augusts reading was the fastest rate of business activity expansion since October 2013.

The services PMI rose to 60.1 from 56.5, which was ahead of expectations of a rise to 57.

The manufacturing PMI edged up to 55.3 from 53.3 in July; the consensus forecast had been for a reading of 54.

The PMIs subtract the percentage of survey respondents reporting a decline in activity from the percentage reporting an increase and as such, a reading of 50 represents the crossover point between an expansion and a contraction in activity.

Higher levels of private-sector output were overwhelmingly attributed to the reopening of the UK economy after the lockdown period in the second quarter of the year and a subsequent increase in both consumer and business spending, the surveys respondents indicated.

"August's data illustrates that the recovery has gained speed across both the manufacturing and service sectors since July. The combined expansion of UK private sector output was the fastest for almost seven years, following sharp improvements in business and consumer spending from the lows seen in April,” said Tim Moore, the economics director at IHS Markit.

"There were encouraging signs that customer-facing service providers have started to catch up with the rebound seen earlier this summer across the wider economy, with easing lockdown measures, staycations and the Eat Out to Help Out scheme all reported as factors supporting growth in August.

"Positive signals for the recovery, of course, need to be considered in the context of UK GDP shrinking by around one fifth during the second quarter of the year. Survey respondents often noted that it could take more than a year to return output to pre-pandemic levels and there were widespread concerns that the honeymoon period for growth may begin to fade through the autumn months,” he added.

The release of the indices has not exactly put a spring in the Footsies step; the top shares index was down 17 points (0.3%) at 5,997.

stellar rises in UK Headline PMI for August, however a closer look reveals: sustained job cuts across the private sector during August. In contrast to the positive trends for output and new orders, latest data indicated the fastest pace of decline in employment numbers since May

— Luke Turpin (@WildboyMarkets) August 21, 2020

9.15am: DCC gently leads the Footsie lower

The FTSE 100 was little changed after a bit of the old “good news/bad news” double act.

Londons index of blue-chip shares was 7 points (0.1%) lower at 6,006.

The good news this morning was that UK retail sales rose by more than expected in July.

Retail sales volumes were up 1.4% year-on-year in July, representing the first annual gain since January.

“Retail sales clearly benefitted in July from a full month of non-essential retailers being allowed to open, pubs, restaurants and hairdressers, all pushing up footfall,” said Howard Archer, the chief economic advisor to the EY ITEM Club.

“However, the opening up of the hospitality sector and other consumer service sectors may have diverted some consumer spending away from retail sales towards services,” Archer suggested.

“Retail sales excluding fuel were up 2.0% month-on-month in July and up 3.1% year-on-year. There was some pick-up in fuel sales as a further easing of the lockdown led to an increase in private transport journeys. Fuel sales rose 26.2% month-on-month in July but were still 11.7% below their February levels.

“Online sales fell 7.0% month-on-month in July as people returned to the shops but were still 50.4% above their February level,” he added.

The bad news was that the UK governments borrowing levels have continued to soar.

“In July the UK government borrowed another £25.9bn, on top of an adjusted £28.8bn in June. In each of the last three months, the amount of money borrowed has been adjusted lower. In April it was adjusted down by £13.6bn, by £9.8bn in May and by £6bn in June,” observed CMCs Michael Hewson.

“Make no mistake these are huge sums of money, with UK government debt now above £2trn, but without some of the furlough money that has been repaid by a host of UK companies, they could have been much higher. This might give the Chancellor some wriggle room as we head into the autumn,” Hewson suggested.

For the first time, UK public debt tops £2tn, about the same market value of Apple ($2tn).#neweconomy

— Antonello Guerrera (@antoguerrera) August 21, 2020

With the macroeconomic news balancing out, blue-chip equities were, to use the old cliché, seeking direction.

DCC PLC (LON:DCC) was one stock sure of its direction; it was the top faller, tumbling 1.5% to 6,666p after Barclays downgraded the sales and marketing group to “equal weight” and slashed the target price to 6,900p from 8,100p.

8.45am: Slow start for Footsie

It was the calm after the storm for the FTSE 100 index, which made a tentative start to proceedings on Friday.

The index of UK blue-chips crept just 5 points higher in the opening exchanges to 6,018.04.

The UK stocks index appears resistant to what is going on in the US, with the Nasdaq Composite hitting a fresh high on Thursday evening.

The depressed state of the equity markets on this side of the Atlantic would hint at the lack of mega-cap stocks here in the UK on the scale of Apple, Amazon or Facebook.

Impervious to the economic conditions, iPhone maker Apple, for example, has breached the US$2tn market cap landmark this week, helping drag the tech-heavy Nasdaq to record levels.

However, the Footsie also appears to betray nervousness around the local economic outlook.

Representative of the problems closer to home was the latest public finances update from the Office for National Statistics. This showed the UKs public debt has breached £2tn for the first time amid a coronavirus (COVID-19) spending binge designed to keep the nation afloat.

There was some better news from the High Street as the ONS said retail sales had risen above pre-pandemic levels in July as a rebound in demand continued. Volumes were up by 3.6% in July, while the official figures revealed sales are now 3% higher than February – the last full month before lockdown.

On the market, there was little in the way of real action. Tentative early buying of Ladbrokes and Coral owner GVC (LON:GVC) pushed the shares up 2.9%.

Bellway (LON:BLWY), meanwhile, was the victim of a Deutsche Bank downgrade to hold amid concerns over productivity levels on its building sites post-lockdown. The negative call appeared to have little impact on the share price, which nudged less than a percentage point lower in the opening exchanges.

Traders appeared more intent on acquiring stock in Bellways rivals, with Taylor Wimpey (LON:TW.) up 1.8%, with Persimmon (LON:PSN) also in demand.

An early loser was DCC PLC, the sales and marketing group, which fell 1.3% after Barclays downgraded its recommendation on the shares to equal weight after failing to see the “upside” for the stock.

Proactive news headlines:

SIMEC Atlantis Energy Limited (LON:SAE) has agreed on a debt financing deal with South Korean financial institution Hana Financial Investment, to fund 100% of the Uskmouth Phase 1 project. The debt facility will provide the company with up to £170mln and Hana will also provide an equity bridge loan. The company and Hana will continue to work closely to refine the financing package during the period until financial close.

Tiziana Life Sciences PLC (LON:TILS) (NASDAQ:TLSA) has been granted a patent over the use of its discovery Milciclib in combination with tyrosine kinase inhibitor (TKIs) drugs for the treatment of hepatocellular carcinoma (HCC) and other cancers. “We are delighted that we now have this key patent on the use of Milciclib in combination with other HCC drugs, including a TKI,” Dr Kunwar Shailubhai, the companys chief executive said in a statement. “Issuance of this patent strengthens our clinical strategy as we move forward with the combination of Milciclib and a TKI for the clinical evaluation of advanced cases of HCC as well as in patients with recurrent HCC after liver transplantation," he added.

Advanced Oncotherapy PLC (LON:AVO), the developer of next-generation proton therapy systems for cancer treatment, revealed that it has drawn down an initial $10mln from the interest-bearing secured convertible facility with Nerano Pharma Limited, details of which were announced on June 29, 2020. Concerning the first drawdown of this facility, the company has as a result paid a commitment fee of $0.6mln to Nerano Pharma. The funds drawn down will be used to further the development of the company's LIGHT system.

Silence Therapeutics PLC (LON:SLN), a leader in the discovery, development and delivery of novel RNA therapeuticRead More – Source

[contf]

[contfnew]

![]()

Proactiveinvestors

[contfnewc]

[contfnewc]